A Comparative Financial Analysis of Dominant Media Groups in Belgium

Author: Manon Verougstraete

Market overview

Belgium’s media market is inherently fragmented, owing to its three distinct language groups, which also constrain its overall size. Media outlets are predominantly split between Flemish-speaking and French-speaking audiences, reflecting the country’s linguistic divide. Beyond these two major groups, a niche German-speaking market exists, catering to the mere 1% of the population whose mother tongue is German. Thus, the media outlets producing content in Flemish and French form the backbone of Belgium’s media landscape and account for the lion’s share of its audience.

Nearly all Belgian media outlets are concentrated in the hands of a limited number of powerful entities. The first category comprises the two publicly-funded broadcasters: the Vlaamse Radio-en Televisieomroeporganisatie (VRT), catering to the Flemish-speaking population, and the Radio-télévision belge de la Communauté française (RTBF), serving the French-speaking community. The administrative boards of both organizations are appointed by their respective regional authorities, ensuring they reflect the composition of regional parliaments.

While there is undeniably a political element tied to their governance, it is worth highlighting that helming such institutions is strictly incompatible with taking on any other political role. This proportional representation among board members is designed to prevent any single party from wielding disproportionate clout over the organizations.

Beyond the public broadcasters, five private conglomerates dominate Belgium’s media landscape. The Flemish-speaking market is primarily controlled by three major players—DPG Media Group, Mediahuis Group, and Roularta Media Group—while the French-speaking market falls chiefly under the sway of Rossel Group and IPM Group.

Each of these five conglomerates is owned by a network of companies. Belgian law requires media companies to publicly disclose their shareholder structures, ensuring transparency to some degree. However, there are no binding legal obligations for these companies to divulge the ultimate, physical owners behind those shares. This opacity makes it particularly challenging to identify the beneficial owner. This lack of clarity is precisely why the profiles associated with this report often stop at identifying the key families known to hold the majority stakes in these media entities.

A significant portion of audience share and revenue derived from media content is predominantly held by the aforementioned groups, creating a stark concentration of influence. This pattern holds true across all forms of media outlets, whether it be television, radio, print, or online press.

Ownership concentration is particularly evident within the TV market. Interestingly, not every private group is represented, while the two public entities wield considerable influence, according to 2023 data from Centrum voor Informatie over de Media (CIM), a Belgian non-profit organization responsible for analyzing media reach within the region. VRT, the Flemish public broadcaster, enjoys a commanding position in its market, drawing in over 39% of the audience. Meanwhile, over in the French-speaking television landscape, the playing field is more competitive. Although RTBF continues to lead the pack with an audience share of nearly 22%, it experiences stiffer competition than its Flemish counterpart. Hot on its heels are the DPG and Rossel groups, co-owners of RTL-TVI, which accounted for 20.83% of the TV market share in 2023.

Within the radio market, the vast majority of stations, including those specializing in news, fall under the ownership of the aforementioned groups. In the French-speaking sector, RTBF has been eclipsed from its former leading position in market share. Dominating the field now are Bel RTL and Radio Contact, both managed jointly by the Rossel and IPM groups, which command the largest audience shares among news-centric channels. Collectively, they capture 25.33% of the market, overshadowing RTBF’s modest 5.37%.

In the Flemish-speaking media landscape, the majority of the print market is held by DPG and Mediahuis, both of which are subsidiaries of larger international conglomerates. DPG has firmly planted its flag in not just Belgium but also the Netherlands and Denmark, while Mediahuis boasts a presence far beyond national borders, operating in Germany, Luxembourg, Ireland, and the Netherlands. Lagging behind these juggernauts is the smaller, distinctly Belgian Roularta group, which caters to both Flemish and French audiences.

On the flip side, the French-speaking media market in Belgium is of more modest proportions and leans less towards international stakes. It is predominantly steered by Rossel, with IPM taking second place. While both players dabble in the French market, their operations remain largely tethered to Belgium.

According to 2023 figures from the Centre of Information on the Media, there has been a notable 2.7% dip in newspaper readership, encompassing both print and digital formats. Meanwhile, the tide appears to be turning as Belgian audiences increasingly eschew traditional media in favor of alternative sources. This shift has left an indelible mark, with the circulation of printed news media in the country slashed by half between 2011 and 2021.

Despite these challenges, turnover has not plummeted dramatically, as prominent publishing conglomerates have managed to mitigate the impact of these market disruptions, at least to some degree. They have achieved this through various strategies. Since 2016, a steady pivot toward digital platforms has proven instrumental. By 2021, digital formats accounted for over 34% of all daily news editions. Alongside this gradual shift to digital, media groups have sought further relief by moderately hiking subscription fees as a counterbalance to declining revenues.

However, this strategy is far from foolproof and presents multiple concerns that undermine its long-term viability. To begin with, these “compensatory measures” inherently have ceilings. Increasing subscription prices risks reaching a breaking point beyond which readers will simply refuse to pay. Complicating matters further, private publishers face stiff competition from public broadcasters, particularly the RTBF, which has come under fire for extending its written news offerings beyond its original remit. As this content is made freely accessible thanks to public funding, private players consider it unfair competition, skewing the playing field to their detriment.

More critically, the wave of digitization has proven insufficient to offset the substantial revenue decline resulting from plummeting print sales and diminishing advertising income. While digital advertising does generate revenue, a staggering portion flows straight into the coffers of tech giants, primarily the GAFAM conglomerate. Deloitte reports that over the last decade, Belgian media has lost between 25% and 50% of its advertising revenue to GAFAM, with Google and Facebook reaping the largest chunk. This statistic becomes even more alarming when one considers that traffic on news websites has doubled between 2015 and 2020. The crux of the issue lies not in audience numbers, but in the fact that the prevailing economic model is financially untenable for private media players.

Belgian media finances map

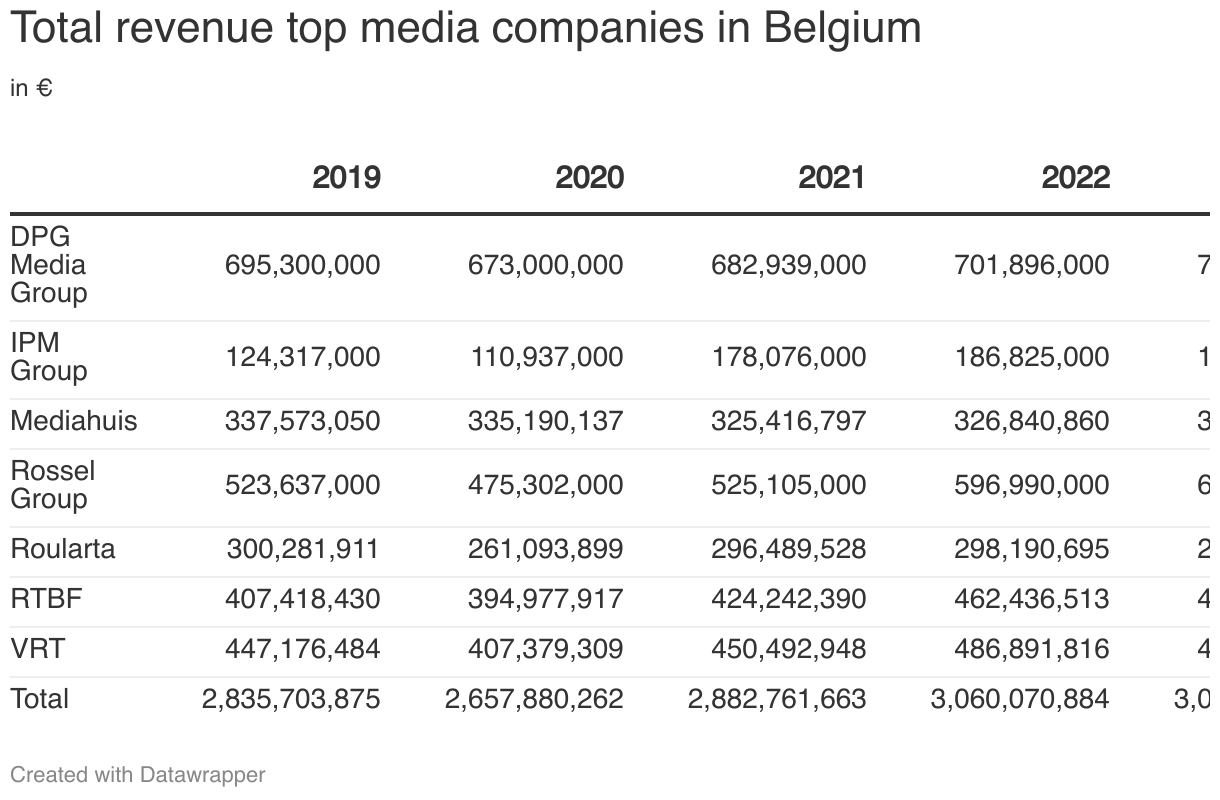

Belgium’s media sector heavyweights have experienced notable expansion in recent years, barring the exception of 2020—the tumultuous Covid-19 year—when revenues took a temporary dip. However, from 2021 onwards, growth has resumed on a yearly basis, culminating in total combined revenues of the seven largest media companies of €3.07bn in 2023. While this represented a modest uptick of approximately 1% year-on-year, it marked a robust 8% rise compared to pre-pandemic levels in 2019.

A lion’s share of these earnings stems from the top five privately-owned media powerhouses, whose aggregate revenue climbed from €1.98bn in 2019 to around €2.1bn in 2023, reflecting a 6% ascent. Meanwhile, Belgium’s public service broadcasters, RTBF and VRT, collectively saw their revenues soar from €854m in 2019 to over €969m in 2023, notching an impressive growth trajectory exceeding 13%.

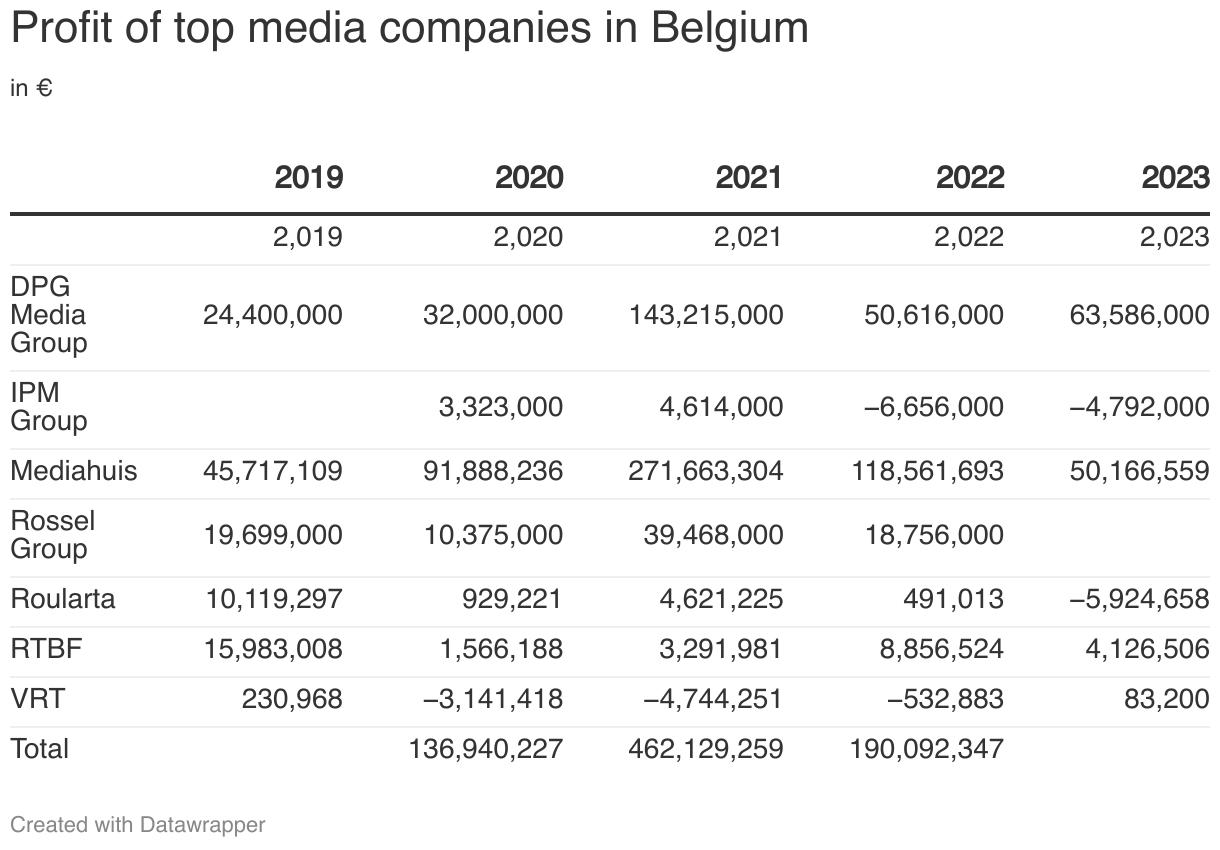

Profitability has also been alive and kicking in the Belgian media landscape. The combined net profits of the five leading media corporations surged by more than 31%, leaping from €138 million in 2020 to just over €181 million in 2022—based on readily available data. All told, the sector’s strong performance underscores its resilience and continuing potential for growth.

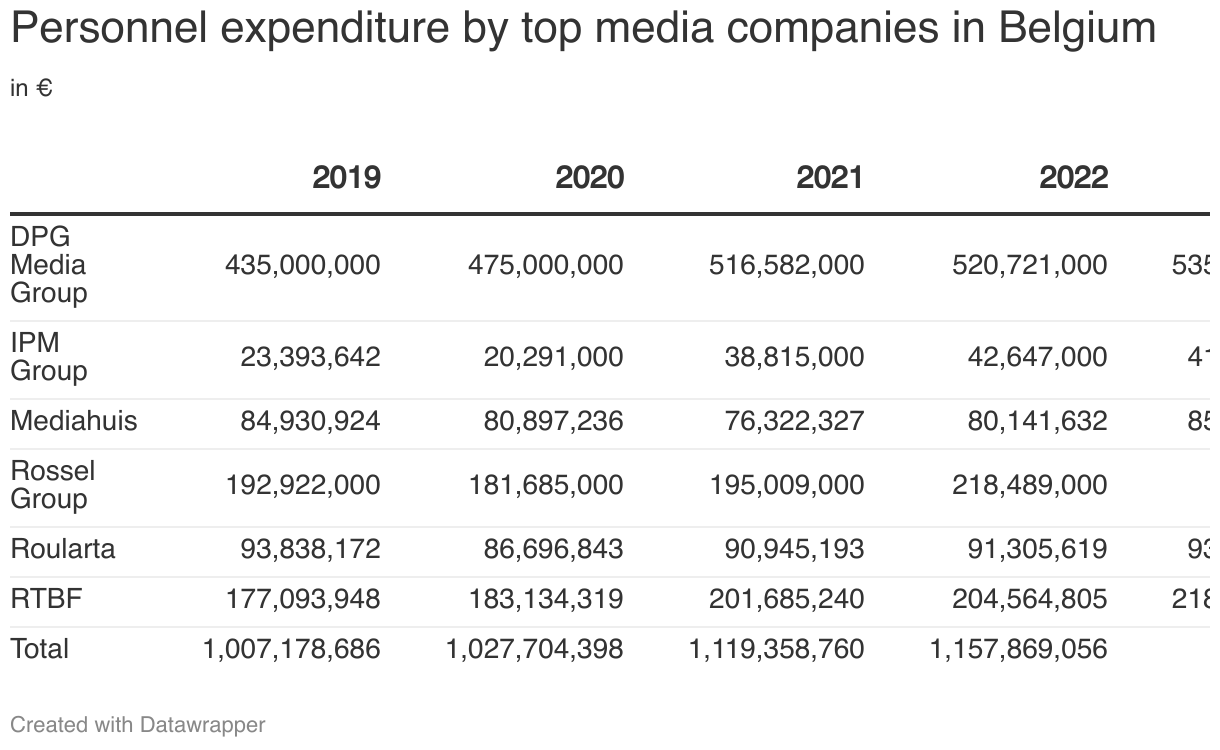

Roughly 40% of the revenue earned by media organizations in Belgium is channeled into personnel costs—a proportion that falls slightly short of the allocation seen in public broadcasters. Take 2022 as an example: the top five private media groups dedicated around 41% of their revenue to staffing expenses, which stood a little shy of RTBF’s more generous 44% in the same category.

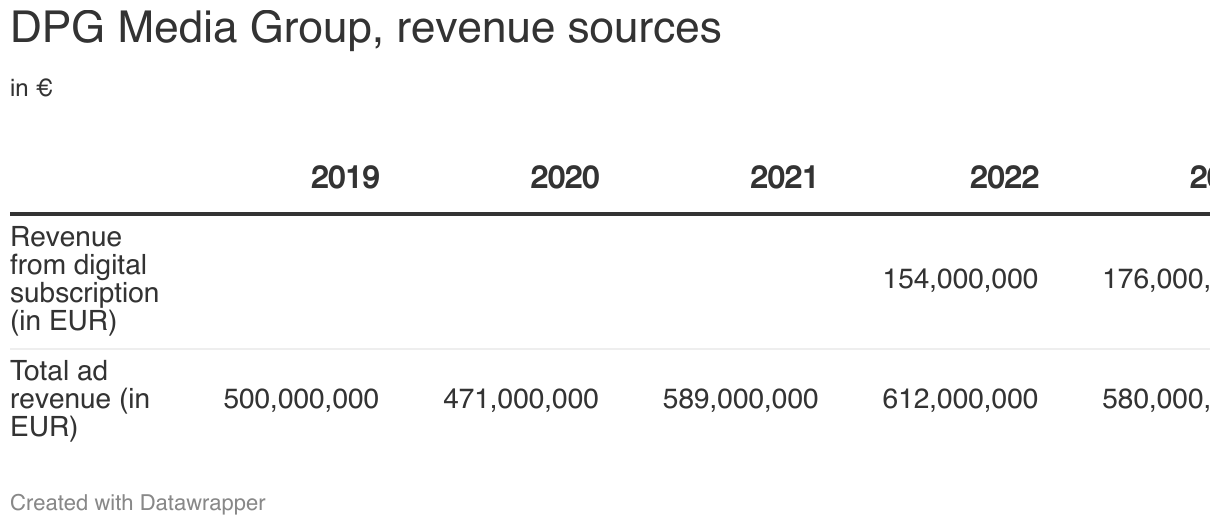

Towering over its competitors in scale and influence is DPG Media, which boasted €705.8m in revenue in 2023. While the company has enjoyed significant clout due to its long-standing dominance, another key pillar propping up its impressive financial success lies in its booming digital ad revenue. Between 2019 and 2023, advertising revenue for the group surged to €207m—a meteoric rise of 250%. At the heart of this growth spurt is DPG Network, an independent platform through which the organization’s “data, subscriber, and advertising systems” are interlinked across all its brands.

This clever synergy enables DPG to dive deep into consumer behavior, harnessing insights to fine-tune its advertising and subscription offerings. The end result is a series of platforms that are not only smoother and more intuitive for users but also designed to keep them coming back for more, hether by content engagement or by committing to paid subscriptions. In other words, DPG’s adept use of data doesn’t just generate spin-off efficiencies—it turns the entire operation into a well-oiled, profit-making machine.

Since mid-2023, this has been particularly evident with the introduction of the Ad Manager self-service tool into the network. Simply put, this tool empowers advertisers to sidestep the traditionally labyrinthine processes entrenched in the procurement platforms of major tech corporations. By building and owning its own advertising platforms, DPG provides advertisers with a lucrative alternative to big tech, as the group possesses deeper insights into the specific content their ads will be displayed alongside. As a result, advertising can be finely tuned to the context at no extra cost because the entire workflow is managed in-house.

There is hardly a parallel to be found among other media groups. While a few emulate certain aspects, their efforts don’t measure up to the same magnitude. Take Mediahuis, for instance—it also offers highly personalized advertising solutions, but these are driven by Ads & Data, an external Belgian advertising agency.

What fuels DPG’s ability to lead this technological charge is its sheer scale. The group boasts a robust portfolio of platforms and publications, creating a compounding windfall effect through strategic investment in shared systems.

At the opposite end of the spectrum lies the IPM group, which finds itself in last place when it comes to both overall revenues and annual profitability compared to the other large players. Several factors culminate in this less-than-stellar performance. Chief among them is their ownership of TV broadcaster LN24, in which IPM acquired a majority stake (over 60%) at the close of 2021. However, in 2022, LN24 posted a net loss of approximately €4m, largely due to stiff competition in the saturated TV market. This arena is dominated by key players such as RTBF—the state-supported public broadcaster—and, more notably, RTL. The latter saw a major shift when it was co-acquired during the same year by its fiercest rival, the Rossel group.

The joint acquisition of RTL—which includes both TV and radio properties—was a game-changer for Rossel and its partner DPG, as they now share equal ownership of 50% each. For starters, RTL boasts an expansive reach, making it a veritable cash cow for its stakeholders. When factoring in its TV channels, radio networks, and broad digital footprint spanning both news and entertainment segments, RTL touches approximately 85% of French-speaking Belgians. Additionally, the collaborative efforts between Rossel and DPG have unlocked the potential for larger-scale investments and opened the door to significant synergies across their television and radio operations—creating a partnership that’s much more than the sum of its parts.

The RTBF factor

For years, editors of French-language media outlets have voiced their discontent over what they see as unfair competition from RTBF. At the heart of their frustration lies the sheer volume of written articles RTBF churns out on its website—approximately 50,000 pieces annually. Backed heavily by public funding—roughly €370m from governmental sources in 2023—RTBF offers this written content free of charge, a practice private media players deem highly uncompetitive. While regulations are in place to curb the scope and length of these articles—including a rule that mandates a sizable portion remain under 1,500 characters—concerns persist about whether these measures adequately level the playing field.

When the details of RTBF’s 2023-2027 contract were unveiled in 2022, prompting outrage from the French-language press alliance, La Presse.be, the group launched legal proceedings to contest RTBF’s mandate in court. Their grievances stem from claims that, rather than tightening existing constraints, the contract appears to have broadened the broadcaster’s leeway. Chief among their complaints is the requirement that all RTBF articles relate to audiovisual programming. They argue that, since the RTBF website qualifies as an “audiovisual activity,” this stipulation is ultimately toothless. Furthermore, an earlier benchmark set by the European Commission requiring that 100% of articles directly connect to television or radio content has been relaxed to 60% in the new arrangement—a shift that only exacerbates dissatisfaction within the private sector.

In October 2024, the Council of State delivered a decisive ruling against the private press outlets, asserting that the contract outlining the RTBF’s roles and responsibilities did not violate their freedom to engage in the written press sector. While the ruling was met with strong condemnation from private media players, others greeted the decision with open arms.

Among RTBF’s advocates, the prevailing argument highlights the indispensable need for a robust public service broadcaster in the confined market of French-speaking Belgium—an institution tasked with challenging the private sector while fulfilling well-defined responsibilities. Proponents of the 2023-2027 RTBF management contract emphasize its critical importance, with the then-Minister for Culture and Media affirming its necessity to protect RTBF’s status as a cornerstone of French-speaking cultural life. The contract, according to the minister, ensures RTBF continues championing Belgian productions, supporting local artists and technicians, and offering universal access to quality information at no charge.

On the flip side of the coin, critics argue that the maintained arrangement represents a looming threat to the sustainability of private media outlets. Such a situation, they contend, may mark not just a blow to the viability of independent news sources but could ripple out, jeopardizing both media pluralism and the overall caliber of news reporting.

Methodology

This study examines the financial and ownership structures of major media conglomerates in Belgium. The groups under scrutiny have been selected based on their substantial size and far-reaching influence, strengthening their position as the central players in the Belgian media sphere. Their inclusion in this analysis offers a panoramic perspective of the country’s media landscape, thus making them instrumental in evaluating the extent of narrative consolidation and its implications for Belgian society.

Foremost among the selected entities are two publicly-owned broadcasters: the Vlaamse Radio-en Televisieomroeporganisatie (VRT), which serves the Flemish-speaking community, and the Radio-télévision belge de la Communauté française (RTBF), catering to French-speaking audiences. Complementing these are five major private players that dominate the Belgian media sector. Within the Flemish market, the heavy hitters are the DPG Media Group, Mediahuis Group, and Roularta Media Group, while in the French-speaking sector, the torchbearers are the Rossel Group and the IPM Group. Together, these organizations paint a comprehensive picture of Belgium’s tightly-knit media ecosystem.

Photo by Mika Baumeister on Unsplash