Revenues and Staffing Within the Romanian Media Industry

By Iulian Comanescu

The economic crisis in 2007-2009 and the rise of online platforms, particularly global social networks, had a significant impact on the Romanian media. Unlike in more developed markets where traditional media’s role as a watchdog of democracy is at risk, the Romanian press can no longer assert itself as the “4th power of the state” or as an important regulatory mechanism in society.

The decline of print media in Romania

At first sight, print media is still distributed and read in Romania. According to BRAT (Biroul Român de Audit al Tirajelor), the Romanian circulation auditor, there are 46 audited titles with a total print run of 501,333 copies. However, it’s important to note that these figures only include five national daily newspapers: Click!, Libertatea, Adevărul, Jurnalul, and Ziarul Financiar. Out of these, two are tabloids (Libertatea and Click!), with a total print run of 64,740 copies. This is in a country with a population of 19.12 million inhabitants1.

Out of the total print run, the two tabloids account for 53,908 copies, leaving the three “quality” newspapers with just over 10,000 copies. It’s worth mentioning that these numbers (averages per issue for the 1st quarter of 2023) do not represent sold or distributed circulation, as the Romanian ABC stopped reporting this data some time ago.

The former distinction between “quality” or “reference” and “tabloid” or “boulevard” newspapers has been erased during the last decade. Serious newspapers are now trying to attract readers (or users of their online editions) with flashy headlines. For example, a title like Libertatea is trying to compensate for the lack of hard news.

The decline of print media in Romania created a vicious circle. Small revenues led to cost cuts, resulting in massive journalist layoffs. As a result, the quality of print media dramatically decreased, driving away even more readers. In addition, the few remaining print titles became strongly biased in political terms, sometimes being taken over by local owners with political connections.

Some of the print media’s audience migrated online, along with the brands themselves, which started investing in spinoff sites with relative success. According to BRAT data, there are a total of 196 audited content sites in Romania, with a combined audience of 233.4 million unique clients in May 2023. While this number cannot be directly compared to the almost 54,000 daily copies in print, the raw difference is significant.

There is a significantly higher number of sites that include hard news, either as online editions of old media brands or as relatively high-traffic independent sites. However, quantity often takes precedence over quality, with hundreds of news items published per day and per site, at a pace close to “churnalism.” Additionally, political bias is frequently observed.

For both media companies and advertisers, online platforms offer a “cheap” alternative to television, which remains the preferred source of news for Romanians, according to opinion polls. Television attracted an average of roughly 3 million viewers per minute in 2023, a decrease from 3.2 million in 2022. However, in a profit-driven broadcast market, public interest and hard news are not prioritized. Instead, high ratings and revenues are generated by entertainment programming.

Revenues comparison: broadcasting versus print+online

Revenues and profitability serve as key indicators of a robust media business that can thrive independently of political influence. Moreover, they also reflect the popularity and societal demand for media content. However, it is important to note that this popularity can be attributed to either public interest or hedonistic aspirations.

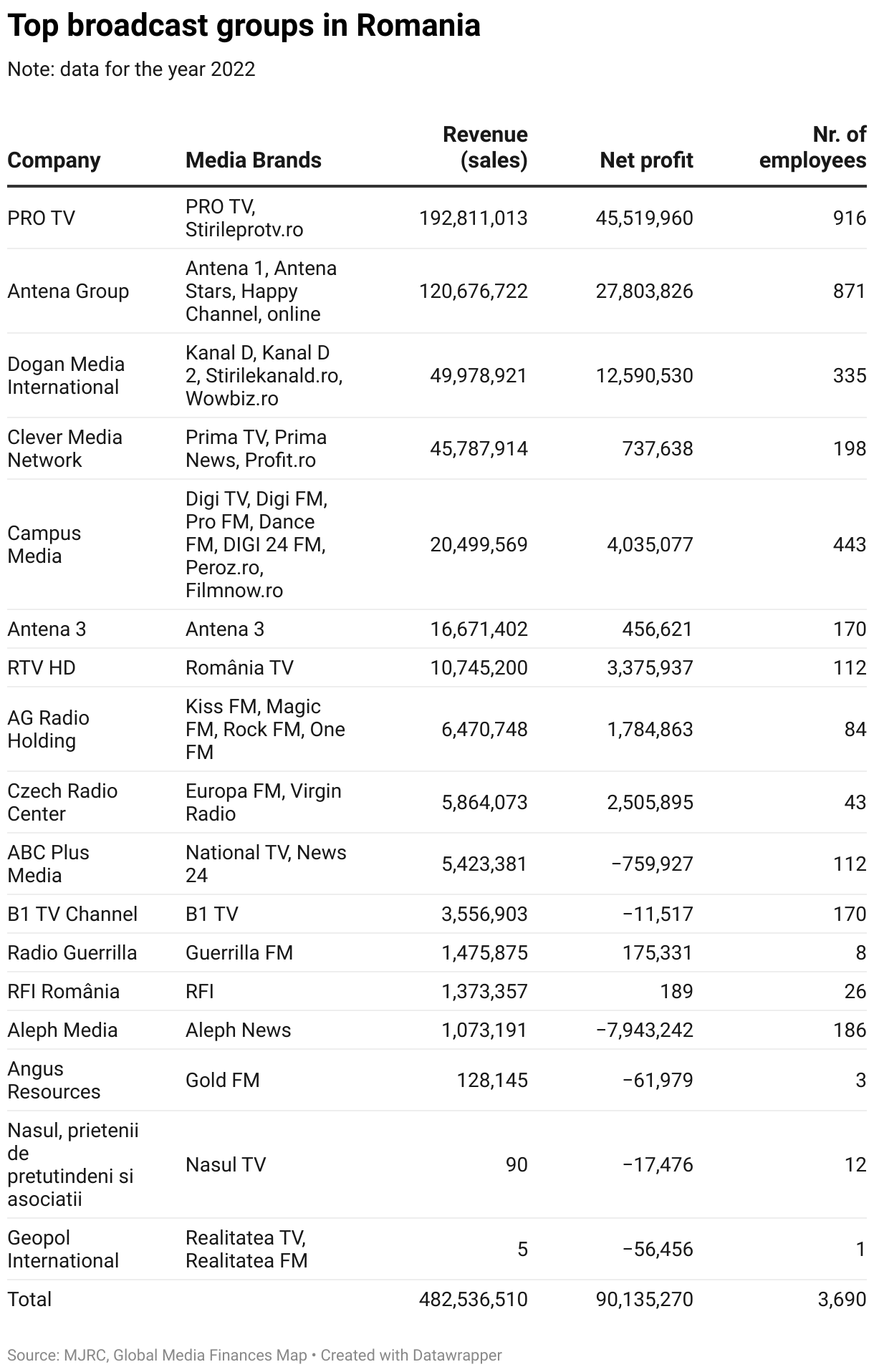

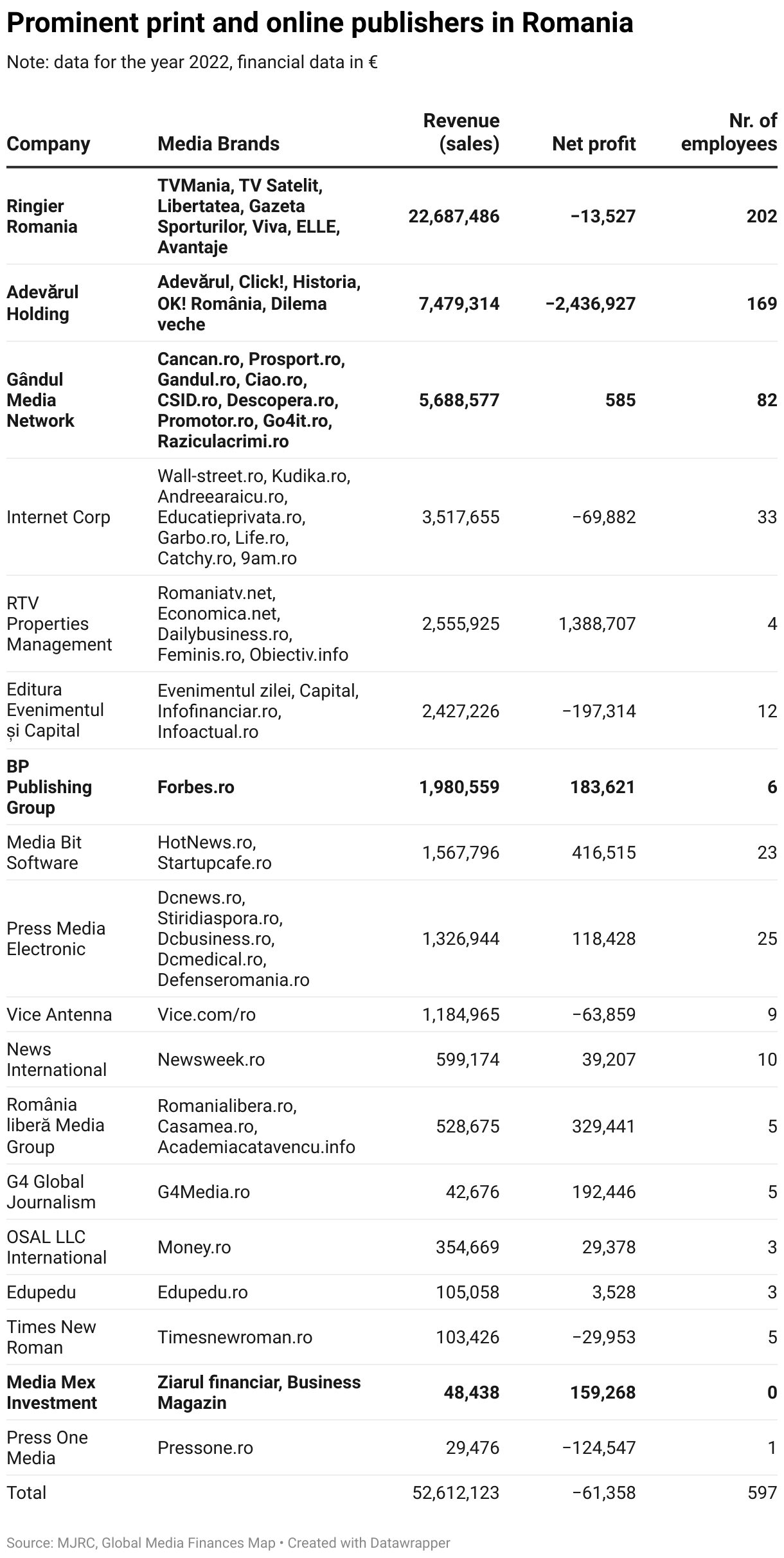

In this regard, the Romanian broadcast market surpasses the print+online market significantly, with revenues exceeding €482m, compared to a mere €53m for print and online platforms.

Only sales were considered to ensure an accurate comparison. The three main commercial television channels (PRO TV, Antena 1, Kanal D) dominate the market, offering a schedule that includes entertainment and news programs that are largely politically neutral (approximately €363m combined out of €482m). The last two broadcasters (Realitatea TV/FM and Nașul TV) have different sources of revenue (donations) or may operate under different companies than the official license owners. The brands mentioned in the table above do not include direct online spinoffs (such as Protv.ro for Pro TV), as they are often operated by the same companies and their contribution to the overall numbers is minimal.

The Romanian public television (TVR/SRTV) has a budget of approximately €90m, with more than 90% of it coming from government subsidies. The public radio (Radio România/SRR) is in a similar situation. However, since their financial data have a different significance, we have excluded them from this analysis.

Print and online media cannot be analyzed separately, as they are often operated by the same companies. However, due to their shared history and the migration from print to online, they can be better interpreted together.

Only the five publishers marked in bold in the table Prominent print and online publishers in Romania still own print titles. Ringier and Adevărul Holding are two of the former big traditional media groups, while other publishers have ceased publishing print editions (România liberă, Evenimentul Zilei & Capital). Some “online natives” (Internet Corp, HotNews) have achieved significant revenues with politically relevant and relatively independent news sites. There are also splinters of the former media groups from 15 years ago, which have been taken over by Romanian owners (Evenimentul zilei & Capital, Ziarul financiar).

However, the print and online content market mentioned above is almost ten times smaller than the TV market in terms of financial size.

A comparative analysis of human resources in the Romanian media

Although broadcast is more resource-intensive, there is a significant difference in the HR markets between broadcast and print+online. Broadcast companies employ almost 3,700 people, while publishers have less than 700 employees combined. Scarcity is evident across the board. Europa FM, the only nationwide licensed broadcasters (the rest of the “national” broadcasters are conglomerates of local licenses), operates with only 43 employees, including technical personnel, along with another radio station, Virgin. RTV Properties Management operates five sites, two of which are business-focused and two are general news, with only four employees. G4Media, a popular and influential political news site, has five employees. There are three employees at Gold FM radio and 12 employees at Nașul TV.

Assuming that one TV channel could go on-air with only one person in front of the camera and another behind it per hour (which is not the case), this would result in a requirement of 36 employees for 18 hours of broadcast per day, a very rough and conservative estimate.

The official data are distorted by various survival strategies employed by the media. Print and online media sometimes pay contributors based on copyright agreements, which are not considered employment. There are also persistent rumors of tax evasion and informal payments, allegedly involving politicians.

Conclusions: comparison with a prominent European publisher

In a comparison with the more lucrative Western Europe market, the dire economic situation of the Romanian media becomes apparent. In 2023, the French media group Le Figaro reported revenues of €570m, with an EBITDA of €47m and an operational profit of €33m, according to data reported by the publisher. Le Figaro, which employs 2,000 people, has higher revenues than the entire combined TV+radio+print+online Romanian markets (€535.1m). Although Le Figaro is a large publication targeting a much larger language market, this comparison is significant in illustrating the financial state of the Romanian media.

One interesting detail is that despite Pro TV’s revenues being roughly a third of Le Figaro’s, Pro TV’s net profit (€46m) is greater than Le Figaro’s operational profit (€33m). Higher profit margins may also suggest scarcity, since they can be obtained by diminishing resources/costs. For example, PRO TV was criticized in the past for the 2nd rate of the international formats broadcast, compared to only a few global superproductions such as “Got Talent”, “The Voice” or “Master Chef”.

With such poor business performance and a scarcity of human resources, the Romanian media can only strive for economic independence, political relevance, and impartial reporting, which are expensive in any market.