Charting Google’s European Footprint: Revenue Streams, Profit Pools and Market Presence

Published: 4 July 2025

Author: Marius Dragomir

Cite this study

Dragomir, M. (2025). Charting Google’s European Footprint: Revenue Streams, Profit Pools and Market Presence. Media and Journalism Research Center: London/Tallinn/Santiago de Compostela.

Abstract

This study examines Google’s financial and market footprint in Europe between 2020 and 2023, drawing on company filings and national statistics from all EU member states where data were available. By assembling and comparing local datasets, the research highlights the uneven distribution of Google’s revenues and profits across Europe, making granular country-level analysis a distinctive strength of the study. The findings show that while revenues expanded steadily, profits declined significantly, reflecting the erosion of earlier tax optimisation schemes, the introduction of new digital levies, and intensifying regulatory oversight. Ireland remains a central hub in Google’s European operations, but its profitability has diminished, illustrating a wider regional shift. Although the study focuses on Google’s performance, the results also speak to broader structural effects on European media markets. The concentration of advertising revenues within Google’s European network leaves most national ecosystems with little financial return, underscoring ongoing pressures on the sustainability of independent journalism.

Keywords: Google, Europe, media, revenues, advertising, regulation

Executive Summary

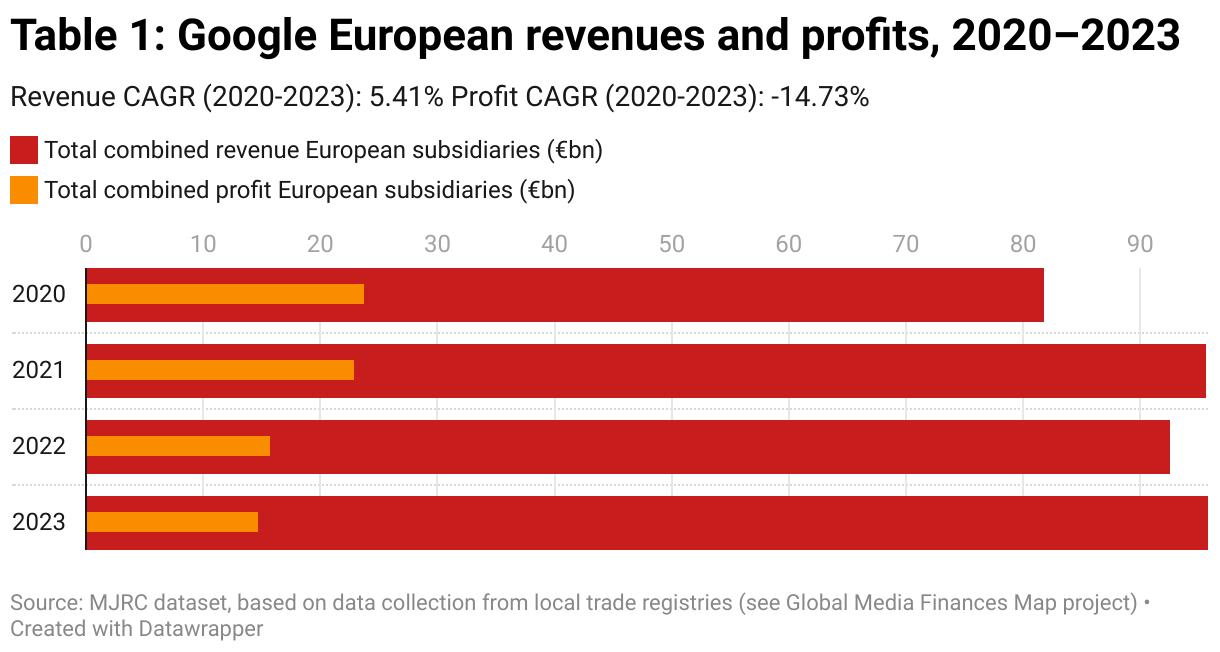

Between 2020 and 2023, Google’s financial performance in Europe exhibited a marked dual dynamic: consistent top-line growth amid significant bottom-line contraction. This trend, while reflecting Google’s continued market dominance in digital advertising and cloud services, also underscores emerging vulnerabilities driven by regulatory, fiscal, and competitive pressures. According to a financial dataset compiled by MJRC (see Table 5: Google operations in Europe, turnover and profits, 2023 versus 2020) from national registries and company filings, Google’s European revenues rose from €81.81 billion in 2020 to €95.86 billion in 2023, yet net profits declined sharply from €23.77 billion to €14.73 billion over the same period.

This asymmetry highlights the shifting structural context in which Big Tech firms now operate. Several interlocking factors—especially the rollout of digital services taxes (DSTs), the end of profit-shifting mechanisms such as the “Double Irish,” and the intensification of regulatory scrutiny—have begun to erode the fiscal advantages that previously buttressed Google’s high-margin European operations. Ireland, historically Google’s European financial center, exemplifies this trend: while its combined revenue from Google subsidiaries increased to €81.5 billion by 2023, reported profits declined markedly, indicating the waning relevance of legacy tax optimization models.

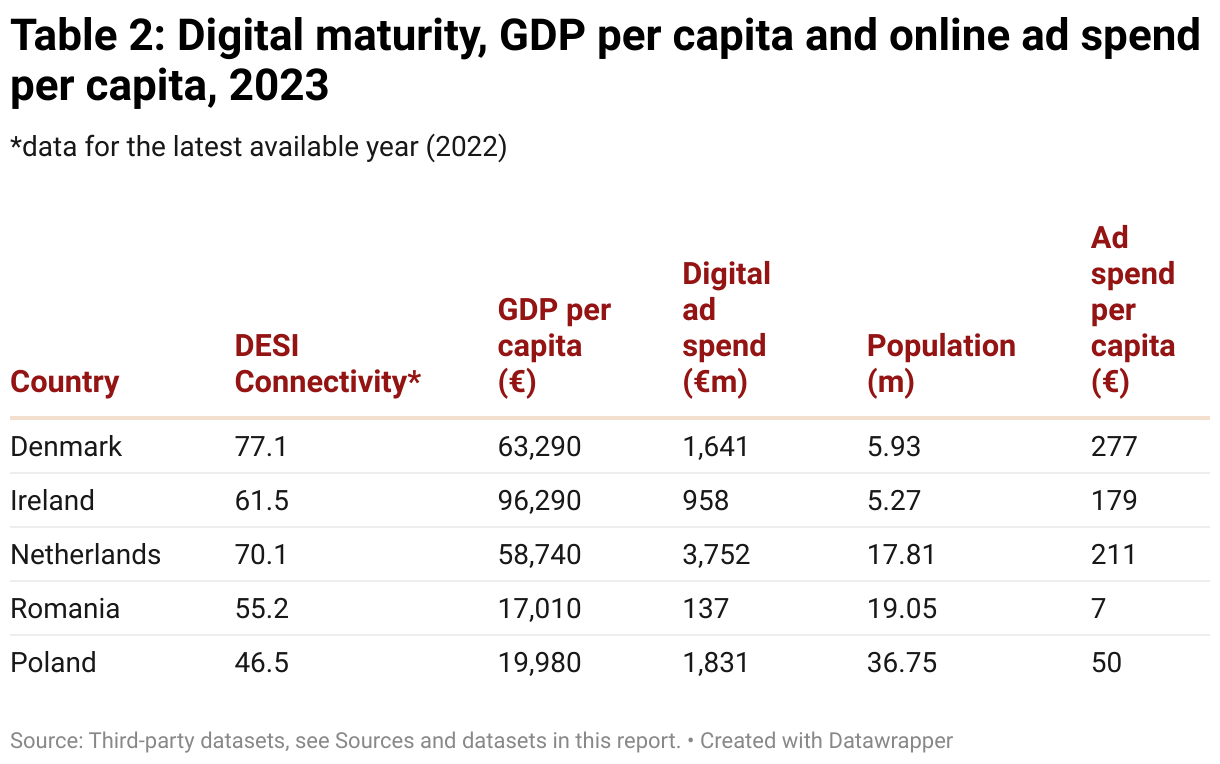

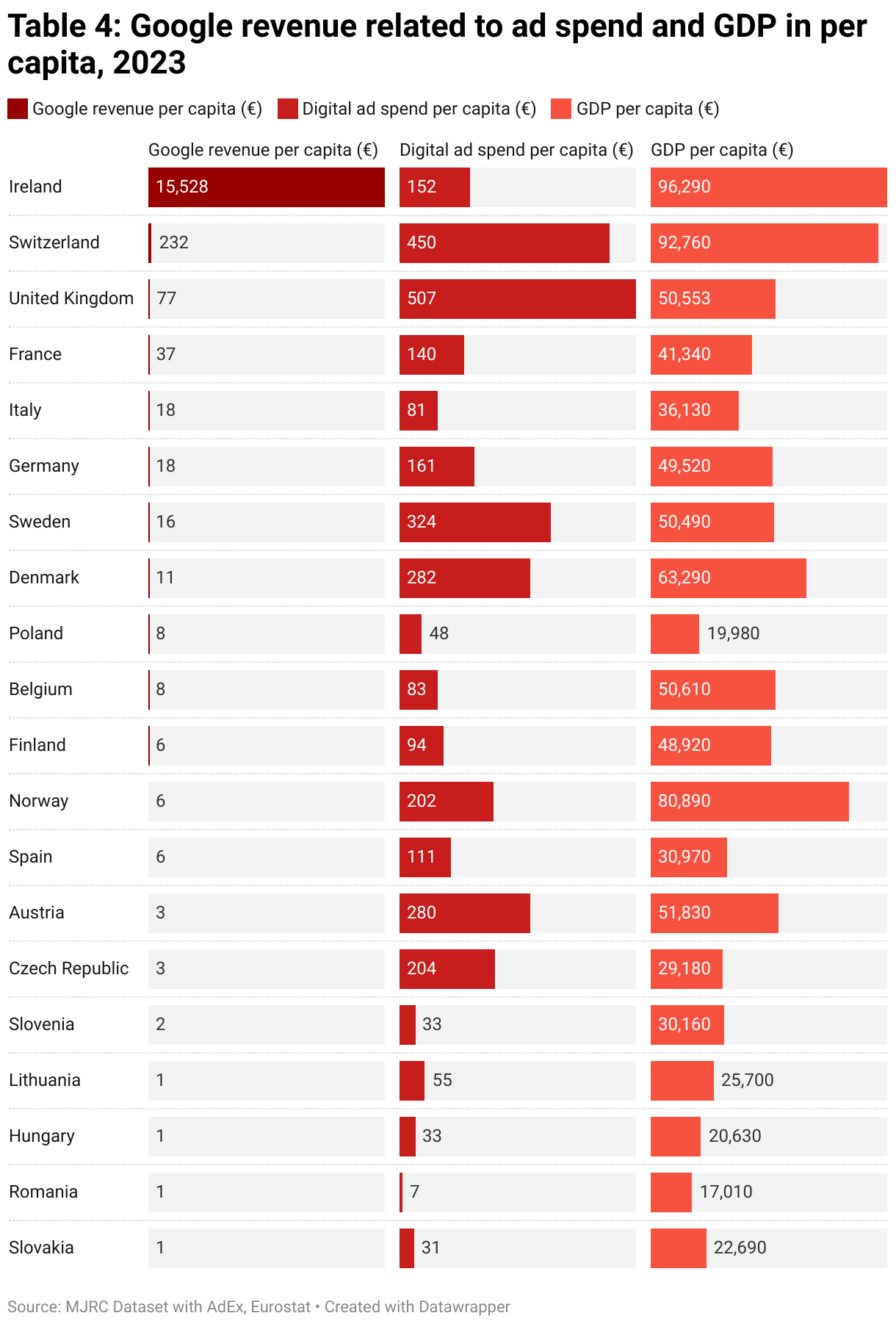

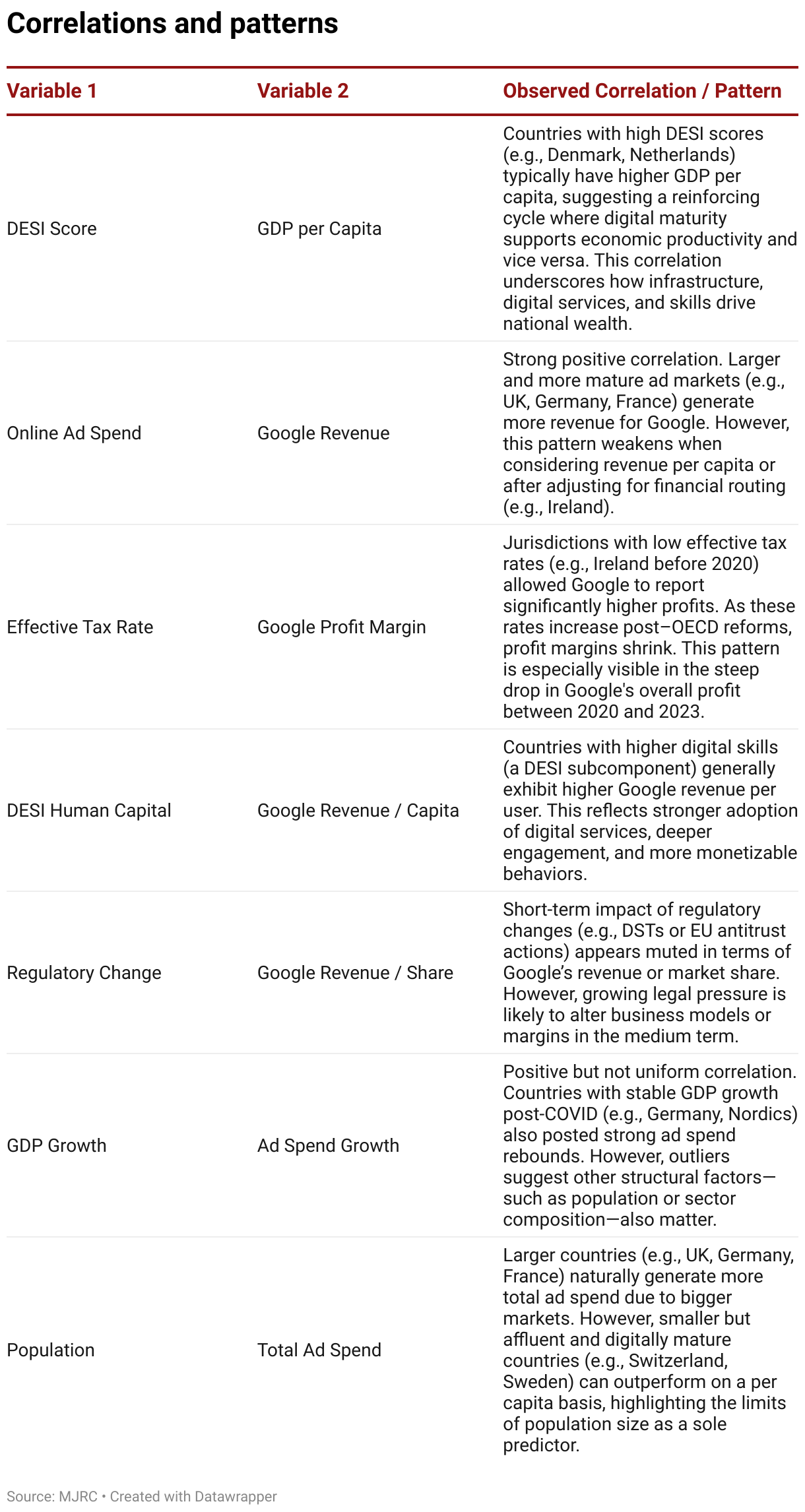

National-level data further reveal how market size, digital maturity, and regulatory environments shape Google’s footprint. In digitally advanced economies like Denmark or Sweden, high Digital Economy and Society Index (DESI) scores correlate strongly with elevated GDP per capita and digital ad spend per capita. Yet these indicators do not translate into proportional Google revenue per user, suggesting continued financial centralization in a few jurisdictions. Ireland’s €15,528 revenue per capita skews the continental average to €799 as most countries register under €50.

A weak correlation between Google’s per capita revenue and national ad spend reinforces the notion that Google’s revenue declarations remain largely decoupled from actual local market activity. Conversely, digital ad spend per capita correlates more strongly with DESI scores[i], validating that local digital infrastructure, consumer behavior and economic maturity drive advertising expenditure. Notably, markets like Germany, France, and the UK combine high digital ad spend and population size to contribute significantly to total European digital ad expenditures—€13.4 billion, €9.5 billion, and €34 billion, respectively, in 2023.

From a media sustainability perspective, this uneven distribution of revenue is troubling. Google’s share of digital advertising continues to grow, consolidating control over key monetization channels such as search and programmatic display. In parallel, national publishers are left with diminished revenue streams, increasing their dependency on a single dominant intermediary. Legal responses have begun to materialize: a €2.1 billion lawsuit filed by major European media groups against Google in 2024 signaled escalating tensions over the platform’s market conduct.[ii]

The relationship between DESI human capital and Google revenue per capita underscores the value of digital literacy and skills in shaping monetization outcomes. Economies with more digitally literate populations exhibit higher revenue per user, pointing to the strategic importance of digital inclusion for long-term economic competitiveness. Moreover, indicators such as GDP growth and population size correlate positively with ad spend, suggesting that macroeconomic and demographic fundamentals still play a key role in shaping digital market trajectories.

In sum, the financial story of Google in Europe in recent years is not merely about growth or contraction, but about transformation. As the regulatory, fiscal, and digital landscapes evolve, so too will the power dynamics between platforms and national economies as well as between tech power and media companies. The coming years will be shaped not only by the strategies of firms like Google but by the capacity of European governments and civil society to create a more equitable and sustainable digital ecosystem.

Profit Growth and Contraction: Insights from the MJRC Dataset

In 2020, at the onset of a global recalibration driven by the COVID-19 pandemic, Google’s combined revenues in Europe stood at approximately €81.81 billion. By 2023, this figure had climbed to €95.86 billion. The compound annual growth rate (CAGR) for this three-year period was calculated at 5.43%, indicating steady if unspectacular expansion. These gains align with Google’s continued dominance in digital advertising and the strategic growth of its cloud services, both of which experienced elevated demand during and after the pandemic years.

Yet this upward trajectory in gross revenues was accompanied by a surprising downturn in net profitability. While Google’s European operations had registered a substantial €23.77 billion in net income in 2020, this had diminished to €14.73 billion by 2023. The negative CAGR of -14.74% paints a more complex picture, suggesting that the expansion in top-line earnings was offset by surging compliance costs, regulatory interventions, and the growing burden of digital services taxes (DSTs) in numerous jurisdictions.

At the aggregate level, these dynamics reflect a strategic environment in flux. European authorities have increasingly scrutinized the dominance of Big Tech firms, especially in relation to their influence on national tax bases. Several countries—including France, Italy, Austria, and the United Kingdom—introduced or expanded DSTs during this period[iii], directly affecting the financial dynamics of companies like Google. At the same time, the rising cost of compliance, data protection, and mounting competition from local infrastructure and regulatory measures have also impacted Google’s margins.

When broken down into national data, Ireland remained Google’s financial epicenter in Europe, with the headline figures for revenues and profits reflecting the combined results of Google Ireland Limited and Google Ireland Holdings Unlimited Company. Google Ireland Limited is Google’s main operational company for EMEA sales and advertising, while Google Ireland Holdings Unlimited Company functioned as the intellectual property licensing and holding entity until the end of 2019, after which it became a holding company only.[iv]

In 2020, the combined revenues of these two entities reached €74.5 billion, with a combined profit of €23.1 billion. By 2023, combined revenues had risen to €81.5 billion, but combined profits had fallen to €14.7 billion. This decline reflects both the impact of global tax reforms—especially the end of the “Double Irish” structure[v]—and Google’s global profit reallocation strategy.

While Ireland’s share of Google’s European profits has declined, other large economies such as Germany and France have seen their relative shares increase. Some smaller markets have posted strong growth rates, but from much lower bases. For example, Google Poland reported revenues of approximately €357.7 million in 2024, with a net profit of €29.8 million, according to data collected by the MJRC from local registries. This marks a substantial increase compared to 2020, when the company recorded revenues of €102.8 million and profits of €6 million; yet, far below the multi-billion-euro scale of Google’s business in Western European markets. On the other hand, Poland’s overall growth trend underscores Google’s expanding presence in Central and Eastern Europe. Similarly, countries such as the Czech Republic and Romania have posted strong revenue growth from smaller operational bases. Romania’s Google Bucharest S.R.L. revenue rose from €7.6 million in 2020 to €59.4 million in 2023, although the entity moved from a small net profit in 2020 to a net loss of €9.1 million in 2023.

Digital Maturity, Economic Structure, and Google’s Revenue Engine

The evolution of Google’s financials cannot be understood in isolation from Europe’s broader digital transformation. The Digital Economy and Society Index (DESI) reveals a clear pattern: countries with higher digital maturity—such as Denmark, the Netherlands, Ireland, and Sweden—also report higher GDP per capita and greater per capita digital ad spend. Denmark’s DESI “Connectivity” score, for example, rose from 43.0 in 2019 to 77.1 in 2022, while GDP per capita increased from €53,040 to €64,730 and online ad spend per capita exceeded €277 by 2023. In these digitally advanced markets, Google’s revenue per capita is highest, driven by a combination of high purchasing power, digital skills, and robust infrastructure.

This correlation is not merely a statistical artifact; it reflects the symbiotic relationship between digital infrastructure investment, economic prosperity and the expansion of digital advertising markets. In Ireland, the rapid growth of Google’s revenues has been matched by a surge in DESI scores and GDP per capita, while in Germany and France, robust digital economies have supported both high levels of online ad spend and sustained Google revenue growth.

The relationship between digital maturity and advertising spend is further reinforced by population and economic structure. Larger, wealthier countries with high digital penetration—such as the UK, Germany, and France—are able to sustain both higher total ad spend and higher per capita spend, supporting a more diverse and resilient media ecosystem. In contrast, countries with lower DESI scores and GDP per capita, such as Romania and Poland, are catching up rapidly but still lag behind in absolute and per capita terms.

Market Power, Media Sustainability and the Dangers of Platform Dominance

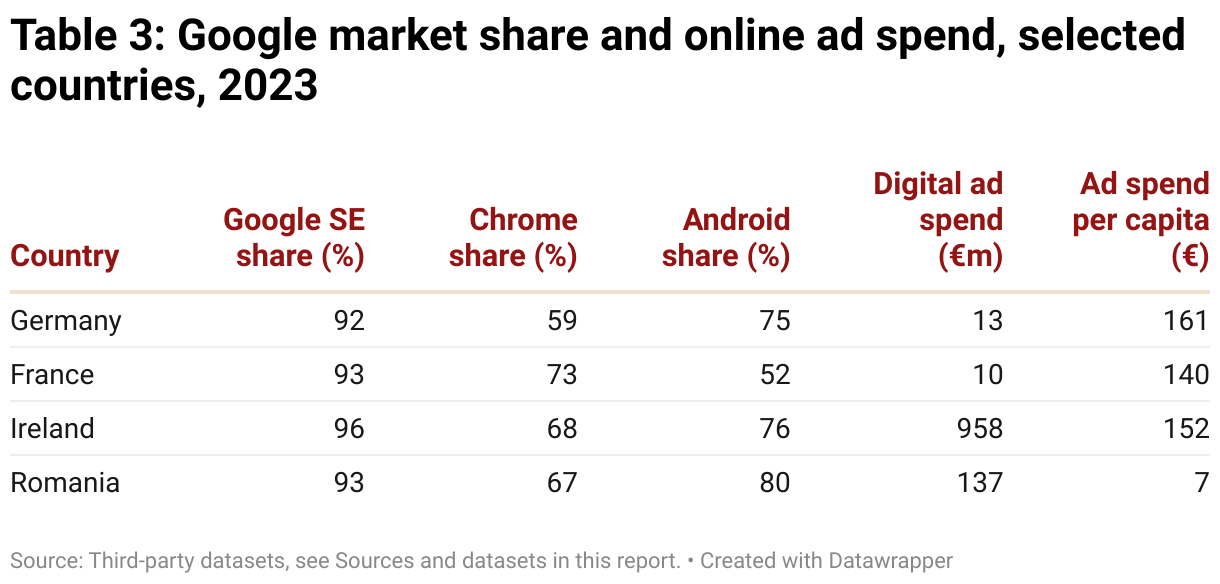

Google’s overwhelming market share—consistently above 88% in search across major European markets—has become both a foundation for its advertising business and a source of concern for media pluralism. In Germany, for example, Google’s search share stood at 92.2% in 2023, Chrome at 58.5%, and Android at 74.9%. This dominance enables Google to capture the lion’s share of digital advertising revenues, but it also raises alarms for Europe’s media and journalism sectors.

The implications for media and journalism are profound. In high-ad-spend markets such as the UK, Norway, Switzerland, and Sweden, robust digital ad spend per capita supports a relatively healthy media ecosystem, enabling publishers to invest in investigative reporting, multimedia content and audience engagement.

However, Google’s dominance in digital advertising poses existential risks for the sustainability and diversity of European media. As Google intermediates a growing share of online ad transactions—often through its own ad tech stack—publishers are left with a shrinking slice of the revenue pie. This is especially true in markets where programmatic and search advertising are the primary growth engines. The migration of ad budgets to Google’s platforms not only reduces the resources available for independent journalism but also increases the dependency of publishers on a single, opaque intermediary.

This concern is not hypothetical. In 2024, 32 major European media companies, including Axel Springer and Schibsted, filed a €2.1 billion lawsuit against Google, alleging that the company’s ad tech practices have eroded their revenues and distorted competition.[vi] The French competition authority has already fined Google[vii] for abusing its dominance in ad tech, and the European Commission’s preliminary findings suggest that Google’s practices may have harmed both competitors and publishers, while increasing costs for advertisers. As digital ad spend continues to grow, reaching €96.9 billion in 2023 across Europe, according to AdEx IAB Europe, the share captured by media companies is under constant threat from Google’s vertical integration and data advantages.

The structure of digital ad spend is also evolving. Video, connected TV (CTV) and digital audio are the fastest-growing segments, with video ad spend rising by over 20% in 2023 alone. For publishers, this shift presents both opportunities and risks. New formats can command higher Cost-per-Thousand (CPM)s and engage audiences in novel ways, but they often require significant investment in technology and skills, and the bulk of programmatic and video ad revenue still flows through Google’s platforms. According to industry estimates, businesses in Europe receive[viii] an estimated €7–8 in GDP impact for every €1 spent on advertising, underscoring the platform’s efficiency but also its centrality—and the risk that Google’s interests may not always align with those of local publishers.[ix]

The dataset illustrates pronounced disparities in how Google monetizes its user base across European markets. In 2023, the average revenue per capita generated by Google across the countries surveyed was approximately €799, according to MJRC calculations. This figure is significantly skewed by Ireland, where per capita revenue exceeds €15,500, reflecting its role as Google’s European financial and licensing hub. In contrast, most other countries report figures well below €50, suggesting that Google’s economic footprint is disproportionately concentrated in a few jurisdictions.

This disparity stands in contrast with digital ad spend per capita, which is more evenly distributed. The average digital ad spend per capita is approximately €164, with top spenders including Switzerland, Sweden, and Germany. However, the correlation between Google’s per capita revenue and national digital ad spend is extremely weak. This underscores that Google’s earnings from European countries are not directly tied to the size of their domestic ad markets, but are instead routed through centralized financial structures — primarily in Ireland.

The Digital Economy and Society Index (DESI) 2022 scores reveal a strong correlation with per capita digital ad spend, but almost no correlation with Google’s revenue footprint. In other words, digitally mature countries (such as the Netherlands, Finland, and Denmark) tend to spend more on online advertising, but that spending does not necessarily translate into proportionate local revenue for Google. This again highlights the structural decoupling of digital market activity and where tech giants actually record their revenues.

Overall, the analysis confirms the enduring impact of regulatory loopholes and cross-border revenue routing, which continue to distort the financial transparency of Big Tech’s operations in Europe.

The Regulation and Taxation Factor

The regulatory and fiscal environment is rapidly changing, with profound consequences for Google’s business model and for the broader digital economy. The OECD’s Pillar Two minimum tax, now enacted in most major European economies[x], is reducing the incentives for profit shifting and leveling the fiscal playing field. Countries with historically low effective tax rates, such as Ireland and Hungary, are seeing a decline in their share of Google’s European profits, with profit reporting becoming more geographically balanced. At the same time, digital services taxes (DSTs) and other targeted levies are raising the cost of doing business for digital platforms, further eroding margins and potentially constraining future investment.

For the media and journalism sector, these changes are a double-edged sword. On one hand, a more equitable tax regime could increase public revenues available for media support and digital infrastructure. On the other, higher compliance costs and reduced profit margins for platforms like Google may translate into tougher negotiations over revenue sharing and less generous support for publisher partnerships. The risk is that, as Google’s margins come under pressure, the company may seek to further optimize its own returns—potentially at the expense of the already fragile media ecosystem.

The broader socio-economic context cannot be ignored. Higher DESI scores are consistently associated with higher labor productivity, lower unemployment and greater personal earnings. Countries advancing in digitalization have seen improvements in employment and personal earnings, while lagging countries show slower progress. Google’s revenue per capita is higher in countries with higher labor productivity and digital skills, reinforcing the link between digitalization, economic growth, and media sustainability.

Markets that weathered the pandemic with greater resilience—Germany, the Netherlands, the Nordics—saw steadier digital ad spend and Google revenue growth, while those hit harder (Spain, Italy) experienced a sharper rebound in 2021–2023. This resilience is mirrored in the ability of local media markets to sustain innovation and audience engagement during periods of economic turbulence.

Conclusions

The findings of this report carry important implications for the future of digital media, platform regulation and economic sovereignty in Europe. While Google’s steady revenue growth affirms its entrenchment as the leading digital advertising player, the significant decline in profits signals a strategic switch in response to shifting fiscal and regulatory headwinds. For media and journalism, the risk lies in further consolidation of advertising power in fewer hands, as publishers face shrinking revenue margins and reduced bargaining power in an ecosystem dominated by vertically integrated platforms.

This power imbalance is exacerbated by Google’s ability to leverage its dominance in search, browser and mobile operating systems to influence user behavior and data capture. As such, even in markets where digital maturity and ad spend are high, local publishers remain financially vulnerable. The recent wave of legal actions against Google by media companies suggests that the tipping point may have been reached. If successful, these cases could reshape the revenue-sharing landscape and create more favorable terms for content creators.

Looking forward, Google is likely to respond to mounting regulatory pressure by further diversifying its European operations, investing in cloud infrastructure, AI services and compliance initiatives. The EU’s Digital Markets Act and ongoing investigations into ad tech practices may force Google to decouple some of its tightly integrated services, potentially opening up space for new competitors and reducing conflicts of interest.

For policymakers and civil society, the key challenge will be ensuring that digital transformation is accompanied by fair taxation, competitive market structures and robust media ecosystems. Investments in digital infrastructure, skills development and independent journalism will be critical to counterbalancing platform dominance.

Sources: National trade registries, NorthData (offers data access to 20 European countries).

Project sources and datasets

Google European Revenues and Profits, 2020–2023 (MJRC Dataset, see profiles on Global Media Finances Map Tech page)

Digital Maturity: DESI

Economic and population data: Eurostat

Ad statistics and data: AdEx

Google Market Share: StatCounter

Effective Average Corporate Tax Rates: OECD

[i] Experts at MJRC employed the Pearson correlation coefficient (r) to quantify the strength and direction of the linear relationship between two variables. In simple terms, they used a standard statistical formula to see how closely two sets of numbers move together—whether high values in one tend to align with high values in the other.

[ii] https://www.theguardian.com/technology/2024/feb/28/news-media-europe-google-lawsuit-ad-revenue

[iii] https://www.cullen-international.com/news/2025/05/Update-on-digital-services-taxes-in-Europe.html

[iv] https://www.netzwerk-steuergerechtigkeit.de/wp-content/uploads/2022/03/Anlage1_Google-Ireland-Unlimited_JA2019.pdf

[v] https://www.reuters.com/article/technology/google-to-end-double-irish-dutch-sandwich-tax-scheme-idUSKBN1YZ12S

[vi] https://www.forbes.com/sites/emmawoollacott/2024/02/29/google-faces-yet-another-challenge-to-its-ad-tech-practices/

[vii] https://www.france24.com/en/business/20210607-french-regulator-fines-google-%E2%82%AC220-million-over-advertising-practices

[viii] https://www.marketingweek.com/advertising-boosts-eu-economies/

[ix] https://www.owm.de/fileadmin/Archiv/public/downloads/publikationen/Value_of_Advertising_-_Studie_D___EU.pdf

[x] https://wts.com/global/hot-topics/pillar-two/pillar-two-implementation-status-worldwide

The complete dataset is available on MJRC’s Exchange — our center’s dedicated workspace and community platform. To request access, click here.

Photo by Kai Wenzel on Unsplash

Artificial Intelligence (AI) Disclosure Statement: The author and his team have used DeepL to translate financial reports from various European registries where we did not have linguistic expertise in-house. All the data were collected manually and double-checked. No AI tool was used in generating the analyis in this study.